I started by living on $30 (Php 1,500) per week and into banking $10,000 (half a million pesos) every month. I am not from the United States nor my parents are rich. I made this happen with grit, determination, and hard work.

I’m on my way to retirement at 30, and I wouldn’t have done it without smart and strategic financial decisions and the support of my loving husband.

So, it’s up to you whether you want to keep scrolling through your social media or stick with me as I share my journey to financial independence.

My First Encounter With Money

I have a Type A personality. I have always been a high achiever, even when I was a kid. I knew how hard my parents worked, with my dad as a farmer and my mom as a factory worker. Being the eldest, I knew that the only way I could help was by listening to them, mostly to my grandma because she was the one my dad was working for.

My grandma always told me that the only way to succeed in life is to study hard so you can get a good job, then work hard and save. I really didn’t understand that much as a 7-year-old, but I did understand one thing: Study Hard.

And that I did.

I remember writing down notes in my notebook using just one pencil. I kept on using that pencil until there was no more lead in the pencil to write with. I always studied hard for quizzes and exams. I also always did my homework.

When I was in Grade 1, we used to have quarterly exams for all the subjects. I would always study hard to make sure I aced every single test.

I recall it was during the second quarterly exam when my teacher asked me to step out of the classroom minutes before we were supposed to start the exam. I went outside with her and asked what was going on.

She told me I could not take the test yet, even though I had already studied for it. I asked her why, and she said, “Your parents haven’t paid your tuition yet.”

I couldn’t believe it. I’ve never really experienced that in my life. My dad always handled it, but I guess this time, he didn’t. I went to the school’s cashier to confirm if my dad really didn’t pay for my tuition for that quarter.

And lo and behold, he didn’t.

I asked the cashier, Mrs. Marcos, whose name I still remember, if I could borrow her phone so I could call my dad. I got her phone, and I called his phone number.

Ring…Ring…Ring…

I was sobbing at this point.

He picked up the phone, and I was crying so hard while telling him that they wouldn’t let me take the test. My dad said he was on his way to school, so I just had to stay put. I waited by the cashier until he arrived.

He saw me and went straight to the cashier. I really couldn’t tell what they talked about. But I knew that I was able to take that test and ace it.

After that incident, I promised myself that I never ever want to be in that same position again. And I NEVER did.

Petite Budget Manifesto

You might have heard of Dave Ramsey’s Baby Steps, Tiffany Aliche’s Financial Wholeness, or Andrew Giancola’s Stairway to Wealth. Those are my inspirations. I took bits and pieces from those financial gurus and modified them to fit my life and goals.

Note that they are made by Americans for Americans. But I am an ambitious Filipina living in the Philippines who happens to have big goals and dreams.

Now, here’s a sneak peek of my Petite Budget Manifesto. I’ll delve into them one by one after this list:

- Petite Budget Abundance Psyche

- Budgeting – Love It, Hate It, Still Do It

- Good Debt & Bad Debt – Don’t Hold Onto Them

- Always Save for the Short Term and Long Term You

- Planning for Retirement – It’s Never Too Early or Too Late to Start

- Wealth Building for Legacy and Giving

- Financial Independence – The Ultimate Goal

Petite Budget Abundance Psyche

What is a Scarcity Mindset?

A scarcity mindset is a way of thinking that believes there’s not enough to go around. It’s like feeling stuck with a limited pie – if someone gets a bigger slice, there’s less for you. This thinking can hold you back from what you want to achieve.

Imagine someone who thinks there are only a few good jobs out there. They might be afraid to take risks or learn new skills because they believe there’s no point – all the good opportunities are already taken.

Fix Your Mindset

The very first thing that any individual who desires to be financially independent needs to do is to fix their “broke mindset” if they have one.

I mentioned in the beginning that I went from living form $30 (Php 1,500) per week to making half a million a month. That is a big difference in a very short span of time.

When you have been living worried about having enough money to buy food for the next day, it is really hard to change your “broke mindset” or “scarce mindset.” I can’t blame you if you are in that situation.

Because I was like that. I experienced having that broke mindset, and I understand how challenging it is to break free.

But if you are someone who lives in a first-world country and has access to the internet, YOU HAVE ZERO EXCUSE NOT TO MAKE IT.

If an 18-year-old Filipina living in a dorm room for $8 (Php 400) a month made it, you definitely can.

It took me 3 months of working overnight at a startup company and studying at the university during the day to figure out how to have the right mindset with money. Once I understand that having something you can offer to help people and have the balls to ask for payment, then there’s no limit to how much you can make.

You won’t be making a million dollars overnight. But, once you get the ball rolling, you can start living far away from the scarcity mindset.

Budgeting – Love It, Hate It, Keep Doing It

Everybody needs a budget. Even millionaires still use a budget. They might not do it line per line like how I do it. But I’m pretty sure that they set specific budgets for all of their endeavors.

What is a Budget?

A budget is basically a financial plan that helps you manage your money. It’s a roadmap that shows you how much money you bring in (income) and how much you spend (expenses) over a certain period, typically a month or a year. The goal is to make sure your spending doesn’t exceed your earnings and that you’re allocating your money toward your financial goals.

Here are some of the benefits of creating a budget:

- Tracks your income and expenses: You’ll have a clear picture of where your money goes.

- Sets and achieves financial goals: A budget helps you allocate funds towards your savings goals, whether it’s a dream vacation or a down payment on a house.

- Avoids debt: By sticking to a budget, you’re less likely to overspend and rack up debt.

Different Types of Budgeting

1. 50/30/20 Budget

This popular method divides your income into three categories:

- Needs (50%): Covers essential expenses like rent/mortgage, utilities, groceries, transportation, and minimum debt payments.

- Wants (30%): Allocates funds for discretionary spending like entertainment, dining out, hobbies, and subscriptions.

- Savings & Debt Repayment (20%): Goes towards building your emergency fund, retirement savings, or paying off high-interest debt.

Simplicity: Easy to understand and implement.

Potential Drawback: Might not be suitable for everyone, especially those with high debt or low income.

I practice this but use a different percentage. I follow the 50% for needs. But since I still have debt I want to pay off as soon as possible, I allot 30% for debt. Then 10% for wants and 10% for savings.

Why do I separate Savings from Debt? I believe that I should always be stashing money away. Even though I prefer to get rid of my debt fast, it helps me sleep well at night, knowing that I have money stacked away in case something happens.

2. Zero-Based Budget

This method requires justifying every expense from scratch for each budgeting period. Every dollar of your income needs to be allocated to a specific category. This approach is good for identifying areas where you can cut back on spending.

- Process: List all your income sources and then subtract your expenses (including savings goals) from your income. Ideally, the sum should reach zero.

Detail-Oriented: Provides a clear picture of where every penny goes.

Potential Drawback: Requires discipline and constant tracking.

I specifically follow this type of budgeting for our personal finance and family finances. I used YNAB to really utilize this. Every time money comes in, we assign a job to every single dollar.

3. Envelope System (Cash Stuffing)

This method involves allocating cash to designated categories (needs and wants) in separate envelopes. Once the cash runs out in a category, you can’t spend more in that category until the next budgeting period.

- Process: Allocate cash to each category at the beginning of a budgeting period (e.g., groceries, dining out). Once the cash runs out, you can’t spend more in that category.

Tangible & Restrictive: Provides a physical limit on spending and discourages impulsive purchases.

Potential Drawback: Inconvenient in today’s digital world and may not be suitable for all bill payments.

I also utilize this method for my emergency funds. I have an envelope for each family expense. Then, I calculate the total spending on that specific expense for a full year.

Why a full year? Because I want a full year of emergency funds. I do not have a fully funded emergency fund yet, but I am getting there.

4. Pay-Yourself-First Budget

This method prioritizes saving and debt repayment.

- Process: Allocate a fixed amount towards savings or debt repayment as soon as you receive your income. The remaining amount is used for all other expenses.

Savings Focused: Ensures you prioritize financial goals upfront.

Potential Drawback: May require adjustments to your lifestyle if a significant portion goes towards savings/debt.

This is one of the most important lessons that I learned in my journey. Typically, when people receive their paycheck, they always prioritize paying their bills and whatever is left would be their savings.

I think this method is so backward. You work so hard to earn that money, and you can’t even prioritize yourself for all those hard-earned dollars.

That’s why I strongly believe that people need to be paying themselves first. Be it saving for retirement, adding more funds to the emergency fund, or even saving for your long overdue vacation. You need to be paying yourself first.

Your bills can wait. You need to make sure that YOU (well, Kathy, in my case) is set up in the present and future. I always make sure that I pay myself first for the short term and for Future Kathy.

5. No-Budget Budget (Track & Monitor):

This method focuses on overall spending awareness without strict categories.

- Process: Track your income and expenses for a period to understand your spending habits. Identify areas where you can cut back and adjust your spending accordingly.

Flexibility: Allows for some spontaneity but still promotes responsible spending.

Potential Drawback: Requires discipline and self-awareness to manage spending effectively.

This is a loose style that the majority of the people I know use. But it is definitely full of flaws and sometimes even leads to further debt, which is a no-go! If you fall off the tracking, you might not even notice that you spent all the money you have, and you’re depending on your credits to supplement until your next paycheck.

Choosing the Right Budget

The best budgeting method depends on your financial situation, personality, and goals. Consider these factors:

- Financial Goals: Are you saving for a house, retirement, or paying off debt?

- Spending Habits: Do you know where your money goes each month?

- Personality: Are you detail-oriented or prefer a more flexible approach?

Personal finance is personal, so it is really up to you to try the different types of budgeting and see what works best.

I am obsessed with budgeting. That’s why I utilize multiple types to fit my needs and goals. And they work for me. But it doesn’t mean that you should also copy what I’m doing. You might get overwhelmed in the beginning, especially if this is your first time.

So, I strongly suggest to pick up any type at your own pace and try them to see which one fits your personality the best and helps you move forward with your goals.

Mastering the Difference Between Needs and Wants

Understanding your needs and wants is key to building a strong budget. Here’s a breakdown:

Needs

Needs are essential expenses that you must cover to survive and maintain your well-being. Not budgeting for them can have severe consequences.

- Examples:

- Housing: Rent, mortgage, utilities (electricity, water, gas).

- Food: Groceries for healthy meals.

- Transportation: Car payment, gas, bus fare, or other means to get to work and essential errands.

- Healthcare: Health insurance, doctor visits, medications.

- Clothing: Basic wardrobe to stay protected from the elements.

Wants

Wants are desirable items or experiences that improve your quality of life but aren’t essential for survival. You can live without them, but they bring you enjoyment.

- Examples:

- Entertainment: Dining out, movies, concerts, subscriptions to streaming services.

- Travel: Vacations, weekend getaways.

- Luxury items: Designer clothing, expensive electronics, high-end furniture.

- Hobbies: Equipment or memberships related to recreational activities.

- Convenience items: Takeout coffee, gym memberships (although some might argue this is a need for health reasons).

Why Budget for Needs First?

There’s a golden rule in budgeting: prioritize needs over wants. Here’s why:

- Financial Security: Needs are the foundation of your financial stability. If you don’t allocate enough for them, you risk falling behind on bills, going into debt, or facing emergencies unprepared.

- Peace of Mind: Having your essential expenses covered reduces stress and allows you to focus on other financial goals.

- Sustainable Spending: Budgeting for needs first ensures you don’t overspend on wants and keeps your finances on track in the long run.

Think of it like building a house. You wouldn’t focus on fancy decor before laying a strong foundation, right? Budgeting for needs is the foundation that allows you to enjoy the extras (wants) responsibly.

Getting Out of Debt Fast

One of the wealth killers is debt. We’ve been so used to living with debt that we don’t even realize how much it is draining our wallets.

Consumer debt is one of the most prevalent debt out there. I think it is highly unnecessary but because of how our society is set up, it makes it really difficult for someone who is just starting out to not fall into the trap of debt.

Debt can significantly impede financial independence in several ways:

- Interest Payments: Debt, especially high-interest debt like credit cards, can lead to substantial interest payments over time. This interest accrual means you’re paying more than the principal amount, which diverts money away from savings and investments that could build wealth.

- Cash Flow Constraints: Regular debt payments reduce your available cash flow, limiting your ability to invest in opportunities, build an emergency fund, or save for retirement. It can also restrict your ability to handle unexpected expenses without incurring more debt.

- Increased Financial Stress: Carrying debt can be a source of significant stress and anxiety, affecting your overall well-being. Financial stress can also impact your decision-making, leading to poor financial choices that further entrench you in debt.

- Opportunity Cost: Money used to service debt is money that could have been invested in assets that grow over time, such as stocks, bonds, real estate, or a business. This lost opportunity can have a long-term negative impact on your financial growth.

- Lower Credit Score: High levels of debt can lower your credit score, making it more expensive or difficult to obtain financing for important purchases like a home or car. A lower credit score can also result in higher interest rates on any future loans, perpetuating the debt cycle.

- Inhibited Savings: Debt repayments often take precedence over saving for long-term goals. This delay in saving can affect major life plans, such as buying a home, starting a business, or retiring comfortably.

- Reduced Financial Flexibility: High debt levels limit your financial options. For instance, you might feel compelled to stay in a job you dislike because you need the income to meet debt obligations, limiting your career choices and personal freedom.

- Risk of Bankruptcy: Persistent debt can lead to severe financial distress and even bankruptcy, which has long-lasting effects on your financial stability and creditworthiness.

To achieve financial independence, it’s essential to manage and eliminate debt effectively, prioritize savings and investments, and maintain a healthy balance between income and expenses.

I’m not perfect. I still have some debt. I used to be very debt-averse. But C*VID happened, and you never know how much you’ll need, especially if you were not living in your home country when that whole fiasco happened.

I used to be so good at not carrying a balance on any of my cards. But when we heard from the Vietnam government that they will not extend our visa anymore and we only have two weeks to prepare, then really expect shiiiiit to happen.

To make this super long story short, we had to spend over $10,000 (half a million pesos) just for flight tickets for the three of us. Then, we have to spend more money on the quarantine hotels. You cannot do Grab deliveries, so our only option is to order from their restaurant, which was ridiculously expensive.

So, one thing led to another, and we didn’t even know that we already maxed out all our credit cards.

But the good news is, we already have a plan on how to tackle this. Hopefully, before I release this Manifesto, our whole debt is already wiped out.

Now, let’s discuss what are the different debt repayment strategies you can use if you have debt.

Debt Repayment Strategies

Debt Avalanche

This method focuses on paying off the debts with the highest interest rates first. By doing this, you save the most money on interest in the long run. To use the avalanche method, list out all your debts and their interest rates.

Then, throw all your extra money into the debt with the highest interest rate while making minimum payments on all your other debts. Once the highest-interest debt is paid off, move on to the next highest-interest-rate debt, and so on.

Debt Snowball

This method focuses on paying off the smallest debts first, regardless of interest rate. The idea is that getting quick wins can help you stay motivated. To use the snowball method, list out all your debts, regardless of interest rate.

Then, throw all your extra money at the smallest debt, while making minimum payments on all your other debts. Once the smallest debt is paid off, move on to the next smallest debt, and so on.

I like to use a combination of the Debt Snowball and Debt Avalanche. I usually start with the least amount of debt, and then the remaining budget for debt repayments will be used for the debt with the highest interest.

I mentioned earlier that when I do my budget, I allot 30% for debt repayment. So, for example, I brought in $1000. I set aside $300 for my debt repayment. If one of my cards has a balance of $60 and the other one with $600, I pay the $60 first for the easy win and the $240 remaining on my $600 debt.

Again, you don’t have to copy how I do my debt repayment strategy. I just shared what works for me, and gave me enough motivation to keep on chipping away at my debt.

The highest debt we had was during that time when we had to fly back to the Philippines, and cost us over $10,000 in credit card debt. For a Filipino like me, that’s a hell lot of money.

I am really motivated to wipe this off, and I am proud to say that we are so close to finishing this debt. I am very confident that by the end of 2024, our slate will be wiped clean.

Always Save for the Long Term and Short Term You

Saving for both the long term and the short term is essential for financial stability and future security. You want to enjoy life, but you also want to be prepared for the future (especially during retirement).

When I talked about the 50/30/20 Budget, I mentioned that I am currently allotting 10% for savings. It’s small right now because I am trying to wipe off the debt as fast as possible.

So what I usually do with my savings is that I prioritize saving for retirement, then for emergency funds, and sinking funds.

For example, I save my first $1,000 for retirement. Once I achieve that, I have a list of Wants Dump (tangible things I would like to buy or experiences I’d love to do) that I pick from as a reward. From the $1,000 savings for retirement, I save another $100 for an item in my Wants Dump. This allows me to enjoy life and not deprive myself of the things that give me joy.

Once I got that item from my Wants Dump, I go back to saving but this time $1,000 for my emergency funds. I repeat the process over and over again.

The most important thing here is I have a retirement financial goal, an emergency fund financial goal, and a sinking fund financial goal. As long as I am on track on those 3 buckets, I can save for short-term bucket list items or work on saving for my 3-5 year goals.

How to Figure Out Your Retirement Number for Long Term Saving

The Trinity Study and the 4% Rule

The Trinity Study, conducted by researchers at Trinity University, looked at historical market data to see how much retirees could safely withdraw from their retirement savings each year without running out of money. They found that a withdrawal rate of 4% of the initial nest egg, adjusted for inflation each year, could sustain a retirement lasting 30 years. This is the basis of the 4% rule.

How to Use the 4% Rule:

- Estimate Your Annual Spending: Figure out how much you spend each year on your current lifestyle. This should include essential expenses like housing, food, transportation, and healthcare, as well as discretionary spending on entertainment and hobbies.

- Apply the 4% Rule: Here’s the formula:

Retirement Savings Needed = Annual Spending / Withdrawal Rate

Following the 4% rule, the withdrawal rate is 4%. So, if your annual spending is $40,000, you would calculate:

Retirement Savings Needed = $40,000 / 0.04 = $1,000,000

In this example, you would need to save $1 million to comfortably withdraw $40,000 per year throughout your retirement, assuming a 30-year retirement period and a 4% average annual return on your investments (adjusted for inflation).

Important Notes:

- The 4% rule is a guideline, and it may not be suitable for everyone. Factors like your life expectancy, investment strategy, and desired retirement lifestyle can impact the amount you’ll need.

- The study assumed a 30-year retirement. If you plan to retire for a longer period, you may need to save more or adjust your withdrawal rate.

- This is a simplified calculation and doesn’t factor in potential changes in Social Security benefits, taxes, or healthcare costs.

Beyond the 4% Rule

While the 4% rule is a good starting point, it’s wise to consider these additional points when figuring out your retirement number:

- Inflation: Inflation erodes your purchasing power over time. The 4% rule historically factored in inflation by assuming a higher overall return on investment (around 7%), with 4% covering your expenses and 3% accounting for inflation. However, future inflation rates are unpredictable.

- Investment Returns: The 4% rule assumes a specific investment return. It’s important to have a diversified investment portfolio that aligns with your risk tolerance and goals.

- Retirement Age: The longer your retirement, the more you’ll need to save. Consider how long you expect to be retired.

- Social Security: Factor in how much you expect to receive from Social Security. This can help reduce your retirement savings needs.

My Retirement Number

One of the most important things you need to know to figure out your retirement is how much is your monthly spending. If you haven’t budgeted and tracked your spending before, now is the best time to start doing so.

As of this writing, our monthly spending is around $3,600 (~Php 210,000). This already includes everything from housing expenses, food, transportation, kids expenses, and other miscellaneous.

Yearly, this equates to ~$43,000

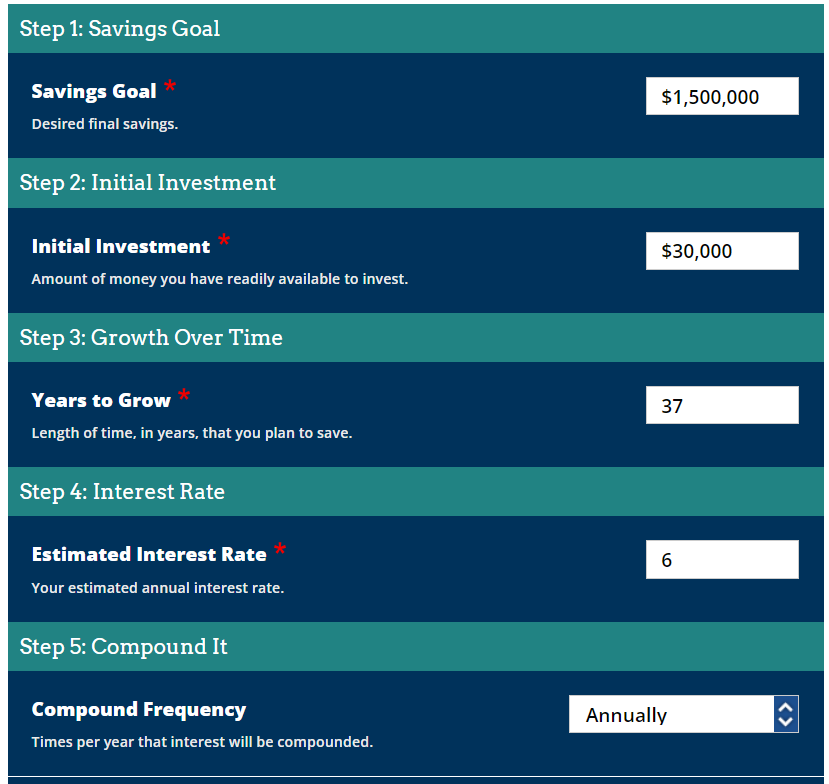

So if I’m 28 years old now and I plan to retire at the traditional age of 65, I would need about $1.5M, assuming I will live until I am 100.

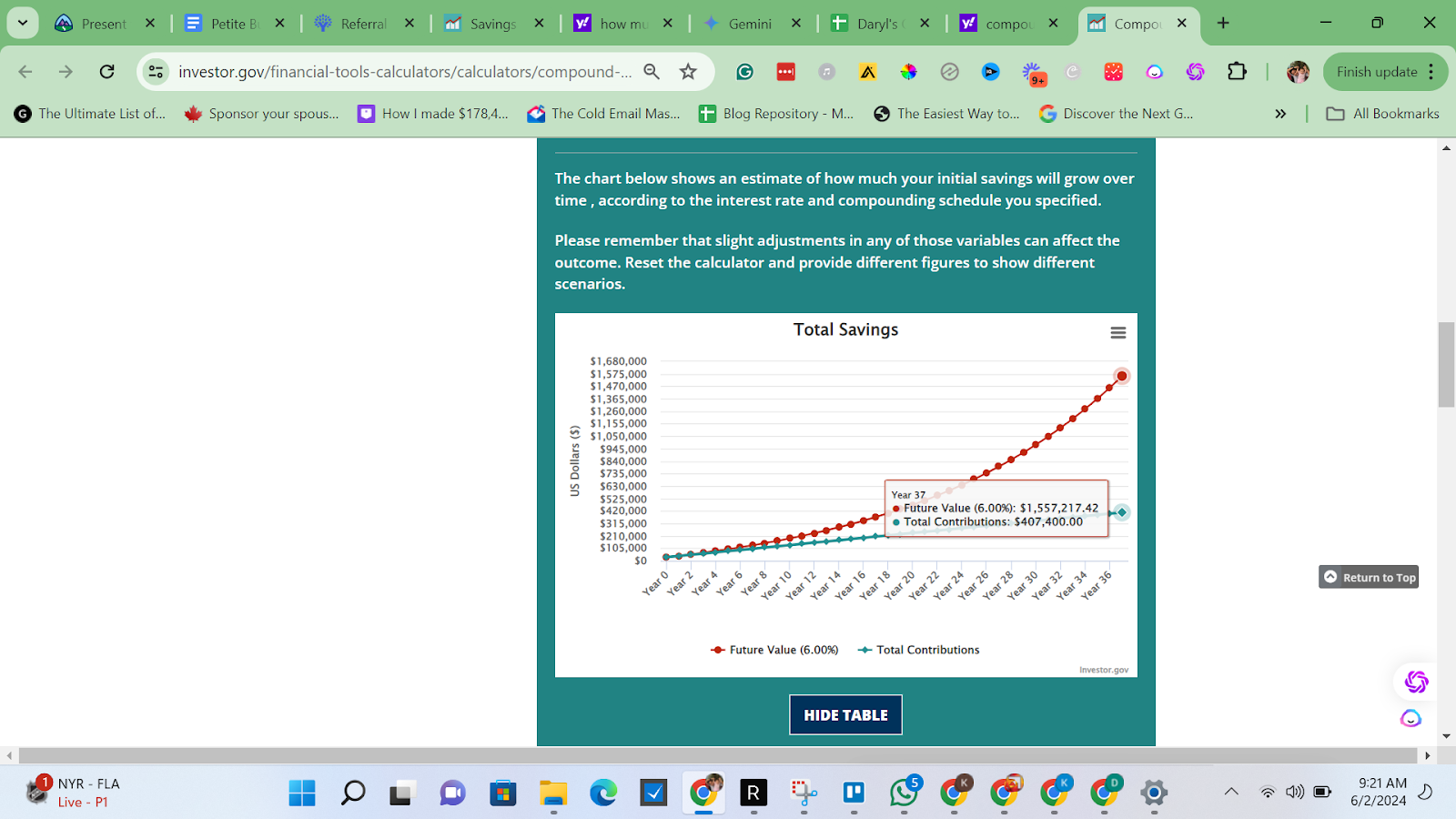

I have diversified investments. Their annual yields vary depending on the investment type. But for this purpose, I will use my Pag-Ibig retirement account which has a 6% interest rate. Let’s use a compound interest calculator to see how much I have to put away every month to have enough to last my whole retirement.

According to this savings goal calculator, I need to save about $813 every month until I’m 65 and reach my retirement number.

My current savings rate is definitely much higher than that. I also utilize different investment vehicles like real estate and index funds, which both have higher interest rates compared to the 6% annual interest rate from Pag-Ibig.

For my stock investments, I’m currently averaging around 12% annually. For the real estate, we are currently doing a buy and hold on two properties. Both of them have already appreciated about 22% in the last 3 years. We also plan on making our primary resident a profitable dwelling my having over 800 plants of dragonfruit to sell.

I probably won’t need to work until 65 to get to my retirement number. I also probably would have to adjust it to be lower because of how we are designing our lives.

I am so grateful that my husband and I are on board with zero-budget living. This means no more mortgage payments, no more utility bills because of solar and wind energy, no more water bills because we’ll utilize a water collection and treatment system, and no more high food expenses because we are growing a food forest.

This may not be an option for some people. But this is the plan that we came up with, and we are both happy and excited about it. Even our daughter loves the idea of raising chickens and planting whatever we eat from the grocery stores.

How to Enjoy Life While Prepping for Your Future You

Now that we’ve covered saving for retirement, which we should start early, we can now discuss the balance we aim to achieve in saving and building wealth.

Striking a balance between future planning and present enjoyment is a key to living a fulfilling life. Here are some tips to help you do both:

Define Your Goals

What do you want your future to look like? Having a clear vision helps guide your actions and keeps you motivated. For our family, we actually formulated our dreams that we review every single week with no fail during our Getting Things Done Family Meeting. Here’s mine:

I have Php 126,000,000.00 in cash with $3k monthly income each coming from Stocks, Rentals, and P2P lending. I also have 500 dragonfruit plants planted for every child. We live in a self sustainable home producing our own food, electricity, and water. I also have a CrossFit gym, laundry shop and snap cafe living a long happy, healthy, joyful, wealthy life surrounded by people who grow with me.

Create an Action Plan

Break down your goals into smaller, achievable steps. This makes future prep feel less overwhelming. If you are a planner like me, you’ll probably get satisfaction from writing down the different financial goals you want to achieve.

Here’s my quick rundown for my savings:

- Emergency Cash

- 1 month

- 3 months

- 6 months

- 1 full year

- Sinking Funds

- Housing

- Malaya

- Food

- Transpo

- Health

- Real Estate

- Leisure

- Travel

I currently reward myself with 1 thing from my Wants Dump for every Php 100,000/$2,000 I save. It could be a small thing like a new running shoes to an elaborate vacation. I do this to keep my motivation and to live this wonderful life I have with my family in the present.

Schedule & Automate

Set aside dedicated time for future planning (budgeting, learning new skills) and automate tasks like saving or bill payments. This is really helpful for those people who still don’t have the habit of saving money.

Having an A Type Personality does not really help me that much with this. I love looking at my finances and knowing where every dollar is going. But I’ve been trying to automate my saving part for small things.

I am currently using GoTyme, it’s a digital bank in the Philippines that allows you to have multiple savings bucket. You can set up savings automation there for daily, weekly, and monthly. You can even automate saving changes to be automatically saved as well in those buckets.

I prefer saving daily as it gives me that daily habit boost.

Remember, life is a journey, not a destination. By finding a balance between planning and living, you can create a fulfilling and enjoyable life for yourself.

Investing for Wealth Creation

Imagine you’re sitting on a beach with your children, building a sandcastle. The tide is low, and the possibilities seem endless. You want this castle to stand strong, a testament to the fun you’ve had together, and a symbol of the future you’re building as a family.

Investing for wealth building is like constructing that sandcastle. You have the beach (your lifetime) to work with, and your kids are the reason you’re building this magnificent structure. Here’s how to make it a success:

Lay a Strong Foundation

The first step is like digging a moat around your castle. You need a long-term view. Remember, you’re not building a sandcastle for tomorrow’s high tide; you want it to withstand the test of time, especially when your kids need things like college or a dream house.

By doing the first 4 steps I laid out so far, you are building yourself a strong financial position. To recap:

- Fix your Scarcity Mindset to Abundance Mindset

- Budget! Budget! Budget!

- No Debt

- Always save for short term and long term. Save for your future you first before anything else.

If you follow those 4 steps, you’ll be ready to start investing for wealth building.

Disclaimer: The information contained within this ebook is for informational and educational purposes only and should not be construed as financial advice. Your financial situation is unique, and the strategies and concepts presented here may not be suitable for everyone. Before making any investment decisions, it is highly recommended that you consult with a qualified financial advisor or professional who can assess your specific needs and risk tolerance. Additionally, this ebook is not a substitute for legal advice. For any legal matters, please consult with an attorney.

By using the information in this ebook, you acknowledge and agree that the author is not engaged in rendering legal or financial services. You assume full responsibility for your investment decisions.

Gather the Best Materials

Just like different grains of sand make a stronger castle, you want a mix of investment options in your portfolio.

Whatever your choice is really depends on your risk tolerance and how fast you want to be financially independent.

I talked about my retirement number earlier. We found out that I have to save about $850 every single month until I am 65 to reach my retirement number.

HOWEVER, if I can frontload my retirement savings to just $410,000, I will not have to contribute another single dollar even more. I would just have to let my money grow until I am 65 years old..

Some options you can get started with for your investing journey are low-cost index funds. They are like the sturdy foundation blocks – reliable and essential.

What are index funds you ask?

Index funds are a type of investment tool designed to mirror the performance of a particular market segment, like a stock market index. Imagine a basket containing a bunch of different fruits. An index fund is like buying the entire basket, where each fruit represents a stock in the market.

Here’s a breakdown of how they work:

- Track a market index: Index funds follow a specific market index, like the S&P 500 which tracks 500 of the largest U.S. companies. By mimicking the index, the fund’s performance reflects how those companies perform overall.

- Passive investing: Unlike actively managed funds where managers constantly buy and sell stocks, index funds take a more passive approach. They buy all (or a representative sample) of the investments in the chosen index and hold them for the long term. This keeps costs low.

- Benefits: There are several advantages to consider with index funds. They tend to have lower fees compared to actively managed funds, offer broad diversification which helps spread out risk, and aim for steady growth over time through the market’s overall performance.

Overall, index funds are a popular option for investors seeking a simpler, lower-cost way to participate in the stock market.

I already mentioned that I am a Filipino but I am a huge fan of Vanguard and Fidelity index funds.

I also have some index funds from Charles Scwabb. And yes, I do not have an American brokerage account, but I can use etoro to buy those.

How about Retirement Accounts?

Retirement accounts are like the smooth pebbles you collect along the shore – they offer tax benefits that make your castle even stronger.

For Those in the United States:

Here’s a list and summary of the main retirement accounts in the United States, including what makes them beneficial and who qualifies to open them:

1. 401(k) Plan

Employer-sponsored retirement plans allow employees to save and invest a portion of their paycheck before taxes are taken out.

Benefits:

- Tax-deferred growth: Pay taxes upon withdrawal.

- Employer match: Many employers match contributions, boosting savings.

- Who Qualifies: Employees of companies that offer a 401(k) plan.

2. Roth 401(k) Plan

Similar to a traditional 401(k), but contributions are made with after-tax dollars.

Benefits:

- Tax-free withdrawals: No taxes on withdrawals if conditions are met.

- Employer match: Contributions can be matched by employers.

- Who Qualifies: Employees of companies that offer a Roth 401(k) plan.

3. Traditional IRA (Individual Retirement Account)

Personal retirement account with tax-deductible contributions and tax-deferred growth.

Benefits:

- Tax-deductible contributions: Lower your taxable income.

- Wide investment options: Stocks, bonds, mutual funds, etc.

- Who Qualifies: Anyone with earned income below a certain threshold.

4. Roth IRA

Personal retirement account funded with after-tax dollars, offering tax-free growth and withdrawals.

Benefits:

- Tax-free growth: No taxes on withdrawals if conditions are met.

- No required minimum distributions (RMDs): More flexibility in retirement.

- Who Qualifies: Individuals with earned income below certain income limits.

5. SEP IRA (Simplified Employee Pension)

Retirement plan for self-employed individuals and small business owners, allowing higher contribution limits.

Benefits:

- High contribution limits: Up to 25% of income or $69,000 (2024 limit).

- Tax-deferred growth: Pay taxes upon withdrawal.

- Who Qualifies: Self-employed individuals, small business owners, and their employees.

6. SIMPLE IRA (Savings Incentive Match Plan for Employees)

Retirement plan for small businesses and self-employed individuals, with mandatory employer contributions.

Benefits:

- Employer contributions: Employers must contribute to employee accounts.

- Tax-deferred growth: Pay taxes upon withdrawal.

- Who Qualifies: Small business owners with 100 or fewer employees, and their employees.

7. 403(b) Plan

Retirement plan for employees of public schools and certain tax-exempt organizations.

Benefits:

- Tax-deferred growth: Pay taxes upon withdrawal.

- Employer match: Many employers match contributions.

- Who Qualifies: Employees of public schools, certain non-profits, and religious organizations.

8. 457(b) Plan

Retirement plan for state and local government employees and certain non-profit employees.

Benefits:

- Tax-deferred growth: Pay taxes upon withdrawal.

- No early withdrawal penalty: Withdrawals before age 59½ are not penalized.

- Who Qualifies: Employees of state and local governments, and certain non-profits.

9. Health Savings Account (HSA)

A tax-advantaged account designed to help individuals save for medical expenses. Contributions, earnings, and withdrawals are all tax-free when used for qualified medical expenses.

Benefits:

- Triple tax advantage: Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- Investment options: Funds can be invested, similar to other retirement accounts, allowing for growth over time.

- Rollover: Funds roll over year to year; there’s no “use it or lose it” rule.

- Who Qualifies: Individuals enrolled in a high-deductible health plan (HDHP). Contribution limits are subject to annual IRS adjustments.

For Those in the Philippines:

Filipinos have several retirement account options to help them save and prepare for their golden years. Here is a short overview of the main retirement accounts available in the Philippines, their benefits, and who qualifies:

- Social Security System (SSS) Pension

- Mandatory pension program for private sector employees

- Provides monthly pension and lump sum benefits upon retirement

- Requires at least 120 monthly contributions and retirement age of 60 years old

- Funded by mandatory contributions from employees and employers

I personally just started contributing to my SSS. Honestly, I don’t think you’ll receive that much at retirement age, given the growth of your contributions. I only like two things about SSS. Number one, the interest rate is fairly low when you get a loan. Number two, maternity benefits. No new mom would like to work after just giving birth, so having just some cash coming in would really help.

- Government Service Insurance System (GSIS) Pension

- Mandatory pension program for government employees

- Provides monthly pension and lump sum benefits upon retirement

- Requires at least 15 years of service and retirement age of 60 years old

- Funded by mandatory contributions from employees and government

- Personal Equity and Retirement Account (PERA)

- Voluntary retirement savings account

- Allows investing up to ₱100,000 annually (₱200,000 for OFWs)

- Contributions are tax-deductible and investment earnings are tax-free

- Can withdraw at age 55 after contributing for at least 5 years

- Open to any Filipino with a Tax Identification Number (TIN)

I started this years ago but I haven’t maxed out my contributions yet. There are many different funds that you can choose from to invest for this program. I personally chose the Growth Equity Fund as I like the aggressiveness of the assets. But I still don’t think I am getting enough growth compared to putting my money in stocks and index funds.

- Employer Retirement Plans

- Retirement plans set up by private companies for their employees

- Can be defined benefit (pension) or defined contribution (savings) plans

- Contributions are tax-deductible for the employer

- Withdrawals are tax-exempt if employee is at least 50 years old with 10+ years of service

- Requires registration with the BIR to qualify for tax benefits

- Investment-Linked Life Insurance

- Combines life insurance protection with investment component

- Allows growing retirement savings while providing insurance coverage

- Withdrawals are tax-free if held until maturity

- Premiums are not tax-deductible

The main goal when investing for wealth creation is to build an investment strategy and keep hammering at it until you can reach your number, until you can reach your financial independence.

This will definitely not be an overnight success. But, small and consistent good habits of saving, avoiding debt, investments, you’ll be able to run this marathon with utmost security and reach the finish line you well deserved.

What does financial freedom mean to me?

It’s not just about reaching a magical number in the bank account. Financial freedom, for me, is about shattering the invisible chains that hold me back from living my best life.

Imagine this: No more scrambling to cover unexpected bills, no more feeling trapped in a job I don’t love because of the paycheck. Financial freedom is the ability to finally say “no” to the things that drain me – the long hours, the toxic work environments, the endless hustle that leaves me depleted.

But saying “no” to negativity opens the door to saying a resounding “yes” to the things that truly matter. It means prioritizing the people who fill my life with joy. Imagine being able to spend lazy mornings with my kids building forts and making memories, or taking them on spontaneous adventures without worrying about the cost. Financial freedom means having the flexibility to support my extended family when they need it most, offering a helping hand without feeling the financial strain.

Ultimately, financial freedom is about owning my time. It’s the freedom to pursue the passions that ignite my soul, whether that’s starting a creative project, volunteering for a cause I care about, or simply taking a long-overdue vacation with my loved ones. It’s the luxury of presence, being fully engaged in every moment with the people who matter most. Financial freedom allows me to stop simply existing and start truly living.

How about you? What does financial freedom mean to you?